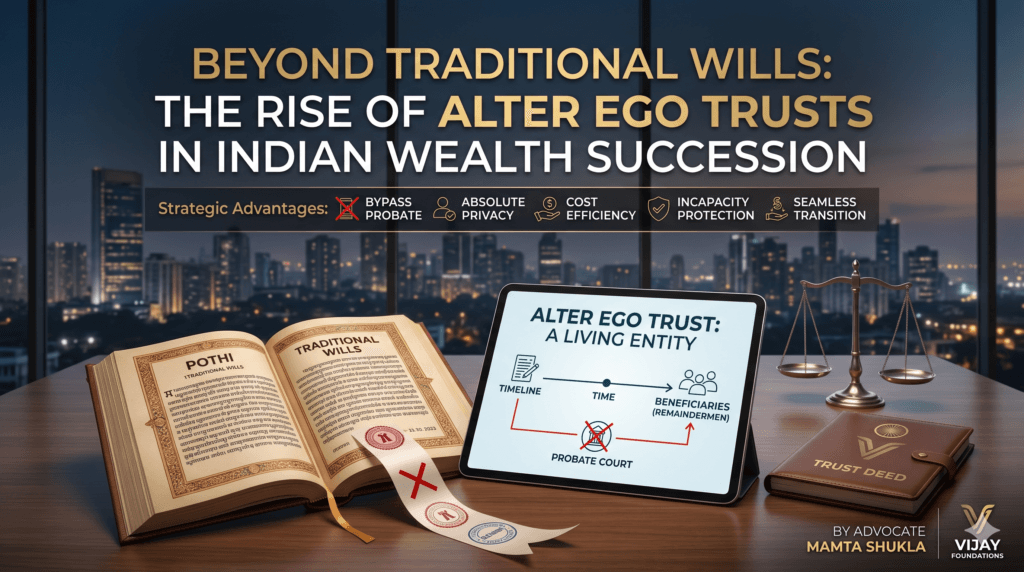

Strategic Alter Ego Trust in India: 5 Reasons UHNIs Move Beyond Wills

As global wealth mobility increases, traditional succession methods are being tested. Discover why UHNIs use this specialized legal structure for absolute privacy and bypassing probate.

As global wealth mobility increases and family structures become more complex, traditional methods of succession planning are being put to the test. For ultra-high-net-worth individuals (UHNIs) and families with cross-border assets, standard wills and family trusts can sometimes expose estates to lengthy court procedures, public scrutiny, and familial disputes.

To solve this, setting up an Alter Ego Trust in India is rapidly gaining traction. It is a highly specialized instrument of succession designed for ensuring absolute privacy, risk mitigation, and seamless asset transfer. However, like any sophisticated legal structure, an Alter Ego Trust in India comes with its own set of regulatory frictions.

Here is a comprehensive look at how these structures function, their 5 strategic advantages, and the compliance hurdles that must be navigated.

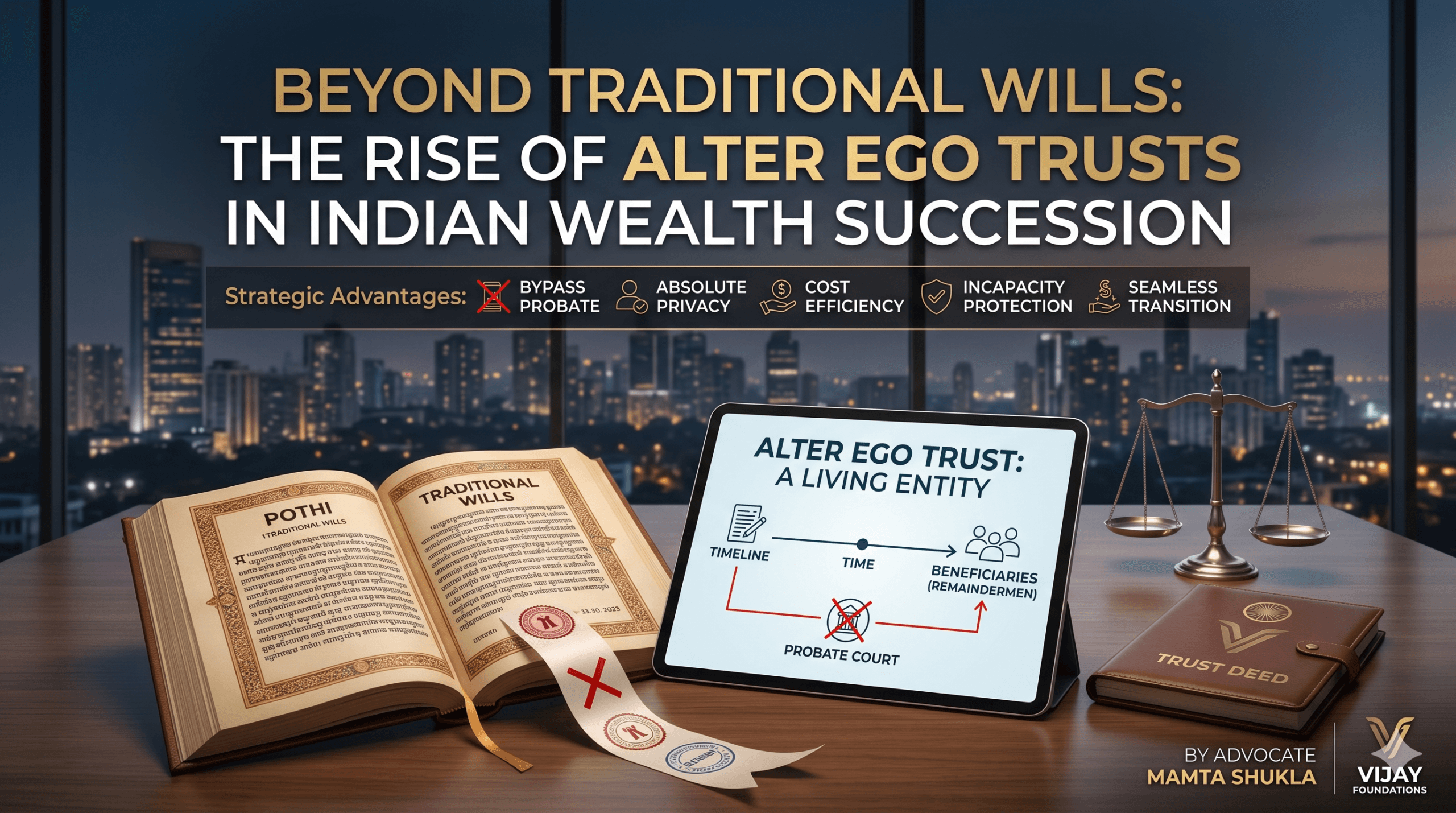

What is an Alter Ego Trust in India?

An Alter Ego Trust in India is a specific type of inter vivos (living) trust. The defining characteristic of this structure is that the individual who creates the trust (the Settlor) is also the primary Trustee and the sole Beneficiary during their lifetime.

In essence, the trust acts as a legal "alter ego" for the creator. The Settlor transfers their personal assets into the trust but retains full control and exclusive use of the income and capital while they are alive. Upon their incapacitation or death, the trust operates seamlessly to distribute the remaining assets to the next generation (the remaindermen) according to the exact terms of the trust deed, completely bypassing the traditional probate process.

| Feature | Traditional Will | Alter Ego Trust |

|---|---|---|

| Publicity | Becomes public record during probate. | Remains 100% private. |

| Execution | Delayed (Weeks to years for probate). | Immediate (Effective upon death/incapacity). |

| Court Intervention | Required (Probate validation). | None (Self-executing). |

| Control | Ends at death/incapacity. | Settlor retains control during lifetime. |

The Strategic Advantages: Why Shift to an Alter Ego Trust in India?

While family trusts have been standard practice for decades, they often require a significant level of disclosure. Structuring an Alter Ego Trust in India offers 5 distinct, structural advantages:

- Bypassing the Probate Process In many Indian jurisdictions, obtaining probate (the legal validation of a will) is mandatory. Probate applications require a comprehensive public listing of properties, bank accounts, shareholdings, and beneficiary names. An Alter Ego Trust in India bypasses probate entirely, as the assets are legally owned by the trust, not the deceased individual.

- Absolute Confidentiality Because the trust is administered privately without the need for court interference or public probate filings, the exact nature of the assets and the designated beneficiaries remain strictly confidential. This is critical for mitigating the risk of public spectacles or predatory litigation.

- Cost Efficiency on Court Fees Probate court fees can be a heavy burden on an estate’s total value depending on the jurisdiction. Transferring assets through a trust circumvents these judicial levies.

- Incapacity Protection If the Settlor becomes incapacitated, a successor trustee named in the deed immediately steps in to manage the assets. This ensures continuity of management without the need to petition a court for guardianship or a power of attorney.

- Seamless Wealth Transition The moment the Settlor passes away, the trust mechanism automatically triggers the distribution to the next generation without freezing bank accounts or halting business operations.

The Operational Risks and Regulatory Friction

While an Alter Ego Trust in India offers unparalleled privacy and seamless succession, it is not without significant friction points. When structuring this kind of wealth transfer within the complex regulatory environment, it is essential to weigh the following drawbacks:

The Stamp Duty Dilemma on Real Estate

Perhaps the biggest hurdle in funding an Alter Ego Trust in India is the transfer of immovable property. When a Settlor transfers real estate into a trust, it is treated as a legal conveyance. This triggers stamp duty, which can range from 4% to 8% depending on the state. Standard family transfer concessions often do not apply, and this upfront cost can negate the financial benefit of avoiding probate fees later.

Weak Protection Against Creditors

A common misconception is that placing assets in a trust automatically shields them from litigation or bankruptcy. Because the Settlor retains total control over the assets and remains the sole beneficiary during their lifetime, courts generally do not view the trust as a separate, independent entity. If the Settlor faces personal legal liabilities, courts can easily "pierce the trust veil" and seize the assets.

Tax Ambiguity and Capital Gains Scrutiny

Under the Income Tax Department of India's framework, there are safe harbors for transfers to standard family trusts (for the benefit of relatives). However, transferring assets to a trust for one's own benefit exists in a regulatory grey area. The tax department may view the initial transfer of assets into the trust as a taxable event, potentially triggering Capital Gains Tax.

Administrative and Compliance Overheads

A trust is a distinct legal entity. It demands rigorous ongoing compliance, including obtaining a separate Permanent Account Number (PAN), filing independent annual Income Tax Returns (ITR), and maintaining meticulous, separate accounting books to ensure personal and trust funds are never commingled.

Potential Loss of Flexibility

To mitigate certain tax implications or lock in succession plans, legal counsel may advise structuring the trust as irrevocable. While this solidifies the estate plan, it means the Settlor permanently surrenders the legal right to dissolve the trust or make fundamental changes if their circumstances change.

Quick UHNI Compliance Checklist

To successfully maintain an Alter Ego Trust structure and avoid regulatory audits, ensure the following foundational steps are meticulously managed:

- Separate PAN Card: Procure a distinct Permanent Account Number exclusively for the Trust entity.

- Independent Bank Account: Never commingle personal funds with trust assets; operate a dedicated trust account.

- Annual ITR Filing: Ensure independent annual income tax returns are filed correctly for the trust.

- Proper Accounting: Maintain meticulous, separate books of accounts, backed by resolutions for major asset transfers.

Conclusion: Is an Alter Ego Trust in India the Right Strategy?

An Alter Ego Trust in India is not a one-size-fits-all solution; it is a highly targeted mechanism. The decision to execute one usually comes down to a clear cost-benefit analysis: Are the immediate costs of stamp duty and annual compliance worth the guarantee of post-mortem privacy and immediate asset continuity?

For liquid portfolios (stocks, mutual funds, cash), the structure is highly efficient and offers incredible peace of mind. For estates heavy in real estate, the upfront friction is often too high. Ultimately, establishing this structure requires rigorous legal drafting and an absolute commitment to ongoing compliance.

If you are exploring succession planning options for your family or business, we recommend exploring our Corporate and Legal Compliance Services at Vijay Foundations to ensure your legacy is future-proofed with precision.